Mining Production and Sales for February 2026

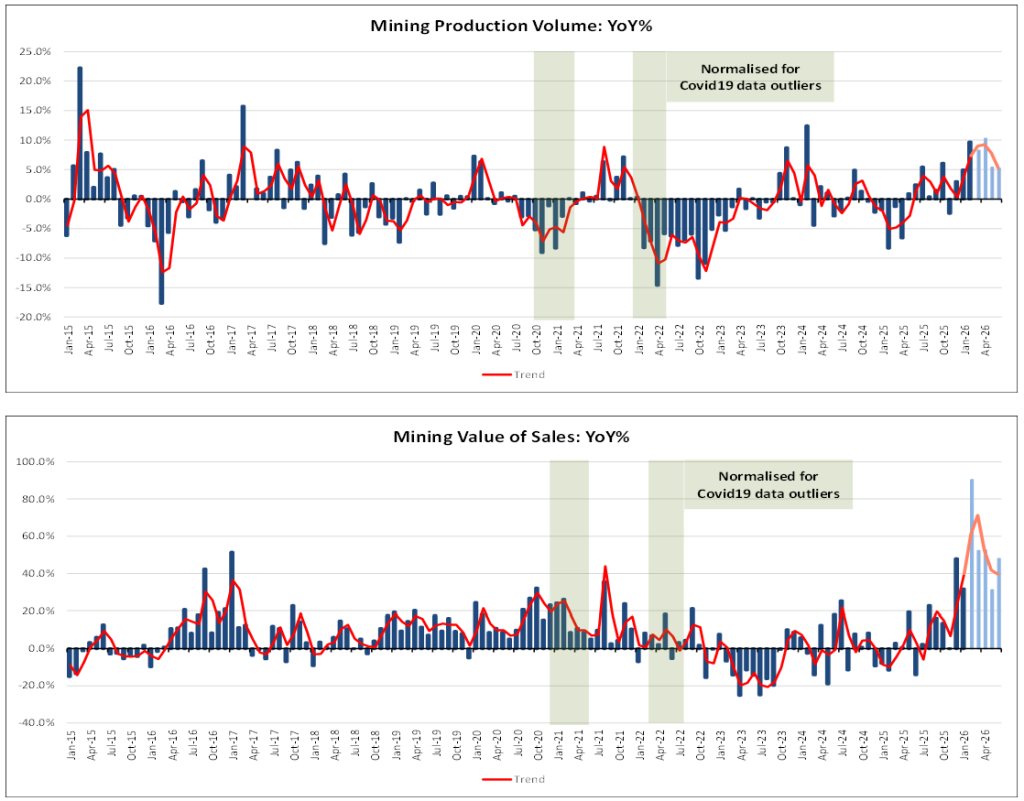

In February 2026, South Africa’s mining activity rose 9.7% following the revised 5.0% increase recorded in January 2026. This growth was predominantly driven by:

- A 52.3% increase in PGM mining production, which contributed 9.4 percentage points to the overall mining output for the month.

- A substantial 26.9% rise in chromium ore output, adding another 1.6 percentage points.

- Manganese production rose by 17.8% during January, while adding 1.5 percentage points towards mining production growth and

- A 12.8% increase in Gold production, which added an additional 1.3 percentage points to total mining output growth for the month.

For the rolling quarter ending February 2026 compared with the previous rolling quarter, seasonally adjusted mining output decreased by 1.7%. This decline was primarily due to:

- A 2.5% drop in platinum mining, which decreased total mining production by 0.7 percentage points and

- Adecrease in Iron ore production, which decreased by 9.7% and, subtracted 1.4 percentage points for the quarter under review.

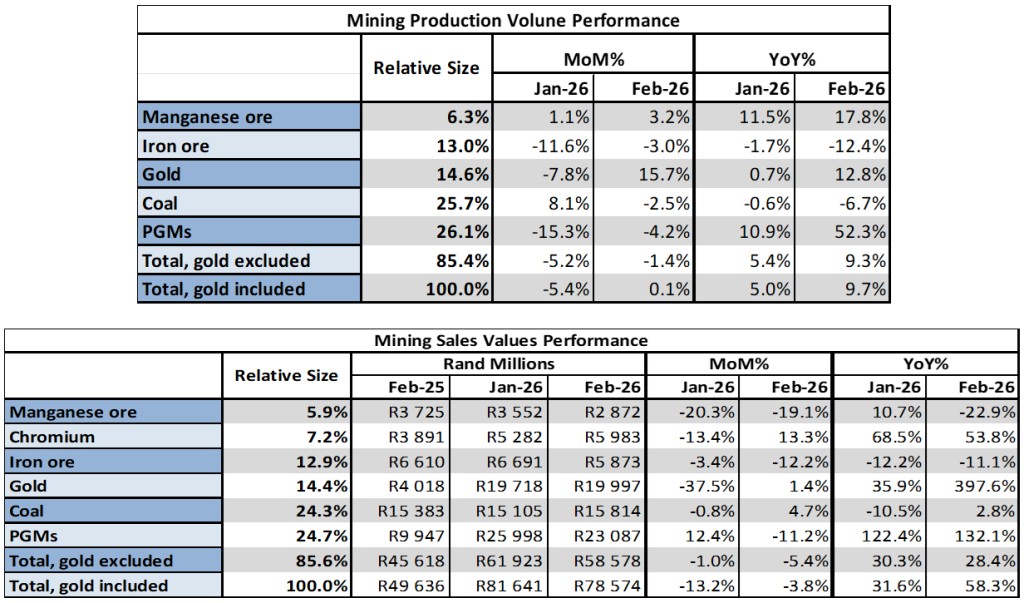

In February, nominal mining sales rose 58.3%. This positive trend was notably supported by:

- A 132.1% surge in platinum sales, which added 26.5 percentage points to overall mining sales growth.

- Another impressive 397% rise in gold sales, contributing 32.2 percentage points.

- Chromium ore sales, which grew by 53.8%, added another 4.2 percentage points.

The mining sector remains vital to South Africa’s economy, generating foreign exchange and employing approximately 444,000 people, a slight decrease of 5,000 from the previous quarter, according to StatsSA labour statistics for the fourth quarter of 2025. According to the latest GDP data, the sector however contracted by 1.3% from the third to the fourth quarter of 2025, with sector growth of 0.9% projected for the first quarter of 2026. This projected first-quarter growth is encouraging, given the sector’s importance to employment and foreign earnings for the South African economy.

Despite a slight decrease in employment from the previous quarter, the sector’s continued significance is evident. However, challenges persist, including concerns over exports to the US following new tariff measures introduced on 7 August, proposed export tariffs on manganese, and import tariffs on steel exports to the Eurozone. The sector also faces challenges related to the loss of AGOA benefits in September and ongoing issues with the new Mining Charter.

On the international stage, geopolitical tensions between the US and China—marked by trade conflicts and tariff disputes—continue to disrupt global markets and limit trade flows. The current Middle Eastern conflict between the US/Israel, and Iran does not bode well for international oil prices as seen in the notable increase in energy prices at this stage, and may cause some sectors to experience rapid cost increases if the conflict isn’t resolved quickly. Nonetheless, some positive developments, such as the continued temporary exemption of certain mining materials used in steelmaking from high US tariffs, have occurred. This provides some relief for the sector, which remains crucial to South Africa’s economy in terms of employment, foreign exchange, and overall growth.