South African Gold and Foreign Exchange Reserves for April 2026

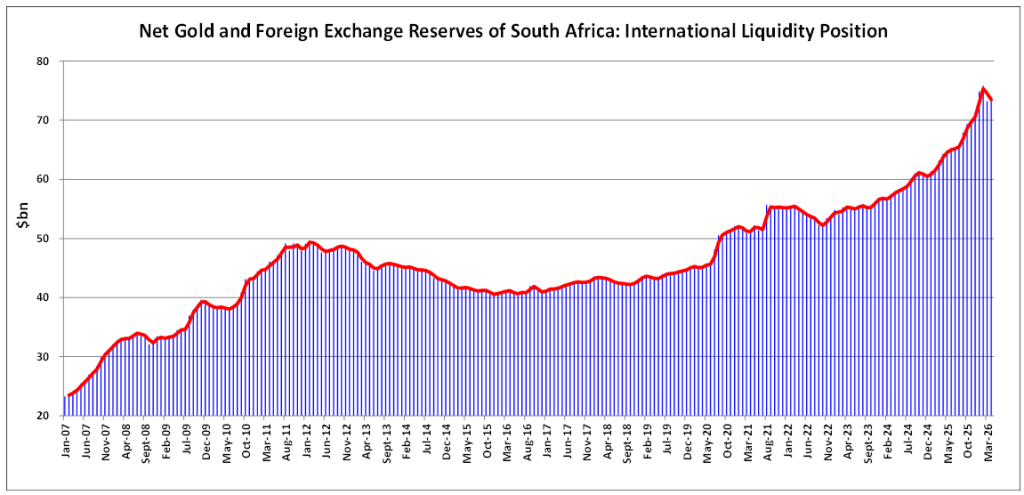

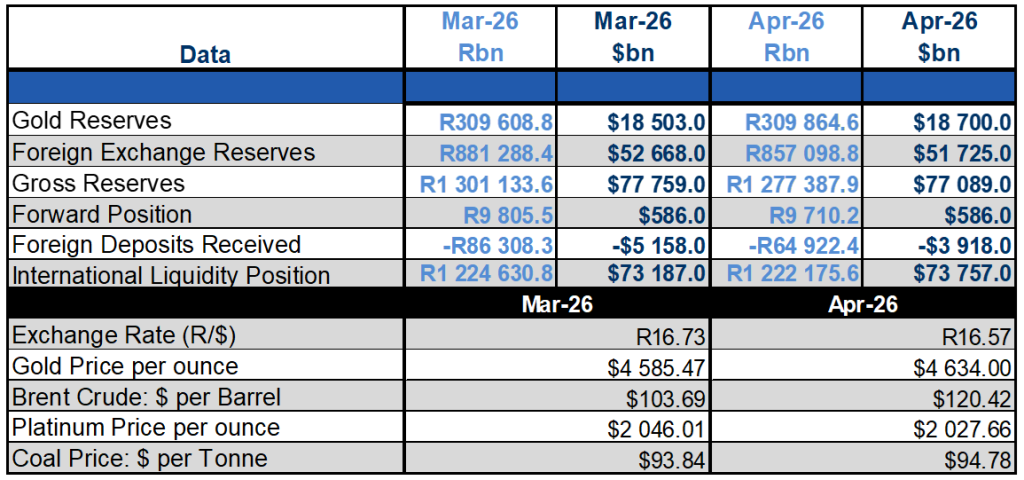

The South African International Liquidity Position, measured by Net Gold and Foreign Exchange Reserves, showed a marginal increase in USD terms but a decrease in Rand terms for April 2026. The Rand appreciated slightly against the US Dollar from March to April 2026 following the outbreak of hostilities in the Middle East, according to official reports from the South African Reserve Bank. Reserves increased by nearly USD 570 million, following a USD 2.6 billion decline recorded in March 2026. The gold price remains high, having increased slightly in April from $4585/oz recorded in March to $4634/oz, and is still 46% higher than the prior year’s price. The sustained high gold price played a significant role in supporting reserves from January through April amid the ongoing conflict in the Middle East.

In USD terms, foreign reserves decreased in April 2026 compared to the previous month. The Reserve Bank continued to sell off some US Dollars in open market operations, partly due to higher prices for imported fuel resulting from the ongoing conflict in the Middle East, thereby impacting South Africa’s net international liquidity position at that time.

Key commodities such as gold, oil, platinum, and coal offer valuable insights into South Africa’s mining sector and inflation outlook. Monitoring these trends is vital for assessing inflation prospects, especially amid ongoing international developments and potential trade restrictions with the US following August’s tariff measures.

Tracking these movements is crucial, as inflation expectations will influence the South African Reserve Bank’s (SARB) interest rate decisions during the second quarter of 2026, especially considering the ongoing conflict in the Middle East and the closure of the Strait of Hormuz. A stable Rand, albeit slightly weaker for now, and notably higher oil prices are conducive to higher inflation. However, global continued geopolitical tensions and possible changes to trade agreements, such as the African Growth and Opportunity Act (AGOA), which has been extended by one year by the US administration, could introduce increased market volatility as the 30% reciprocal tariffs remained intact on South African exports to the US market in general. With recent US tariffs and the Federal Reserve’s decision to hold interest rates steady at its 29th of April 2026 announcement, the Rand may continue to experience short-term fluctuations, which could affect South Africa’s economic outlook for the remainder of the year.