Private Sector Credit Extension (PSCE): March 2026

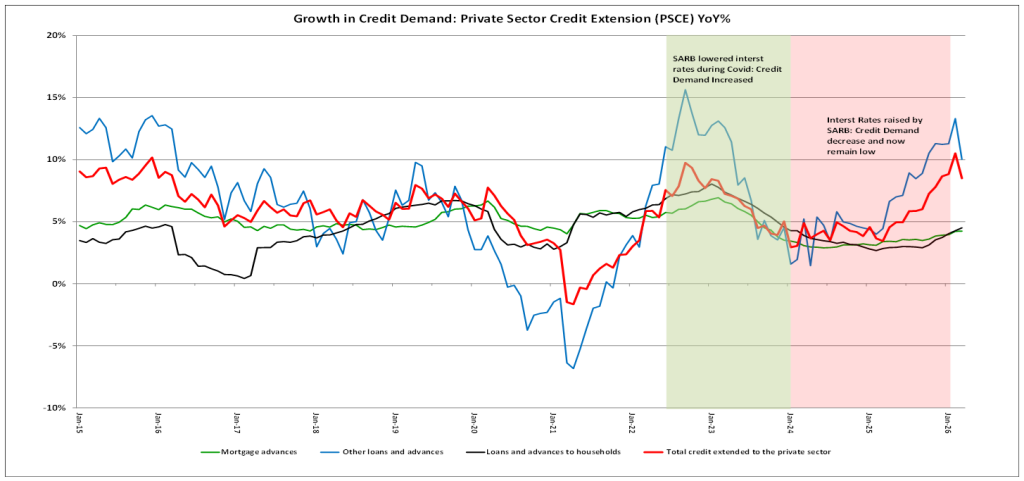

In March 2026, credit demand grew by 8.5%, slightly below the market’s expectation of 9.0%. Since interest rate cuts began in September 2024, overall credit growth has accelerated, with most subcategories experiencing increases, especially following the South African Reserve Bank’s decision to lower interest rates.

Despite these reductions, mortgage advances and credit for acquiring fixed assets remain low, albeit slightly higher than the 3.2% average over the last couple of months. The South African property market is sluggish, reflecting low capital expenditure from both households and businesses. This sector’s recovery remains slow due to high consumer debt levels, low wage growth, and rising living costs, especially household fuel expenditure due to high international oil prices, as well as high administered prices such as water, electricity, and municipal rates & taxes. However, the benefits of lower interest rates are expected to become evident later in 2026; this scenario may change due to inflationary pressures from the ongoing international conflict in the Middle East and higher oil prices as a consequence.

In March, instalment credit sales increased again by 0.9% from the previous month, marking an annual growth of 9.0%. Over the past two years, consumers have increasingly relied on short-term credit to manage rising living costs, as shown by an 10.0% increase in other loans and advances, slightly down from 13.3% in February 2026 figures.

With inflation remaining under control for now, but higher fuel prices at the pump and inflationary pressure due to higher energy costs may cause the SARB to increase interest rates sooner rather than later, which ultimately will influence consumer demand in an adverse manner.