Mining Production and Sales for April 2026

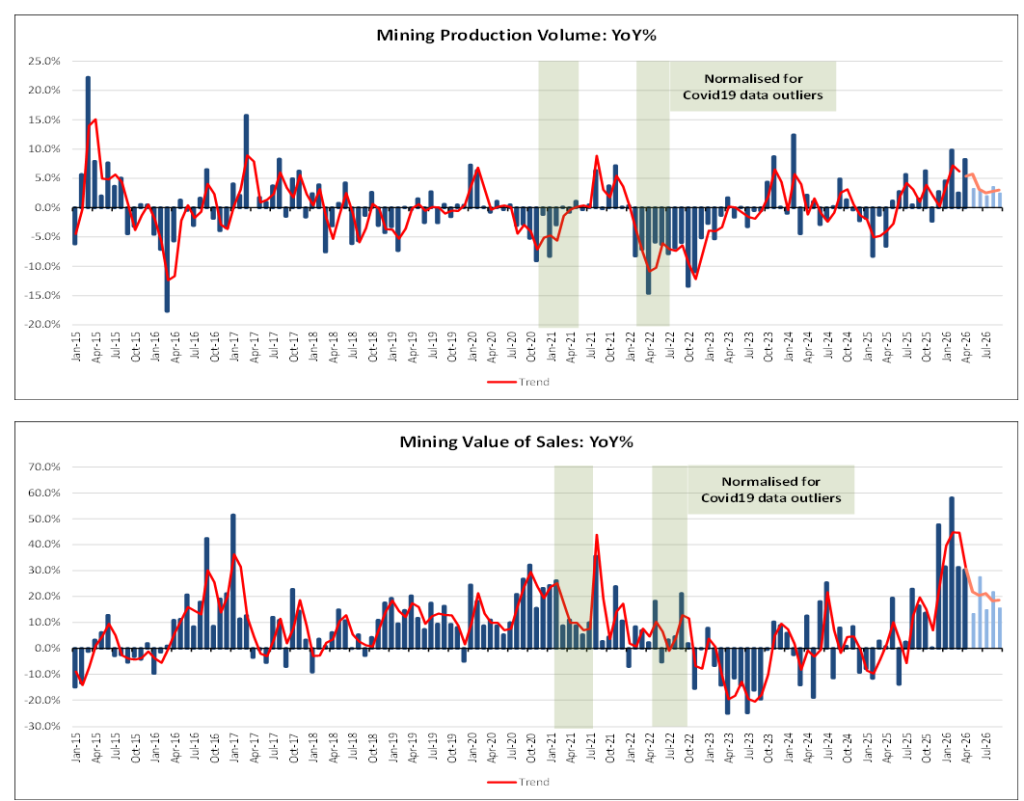

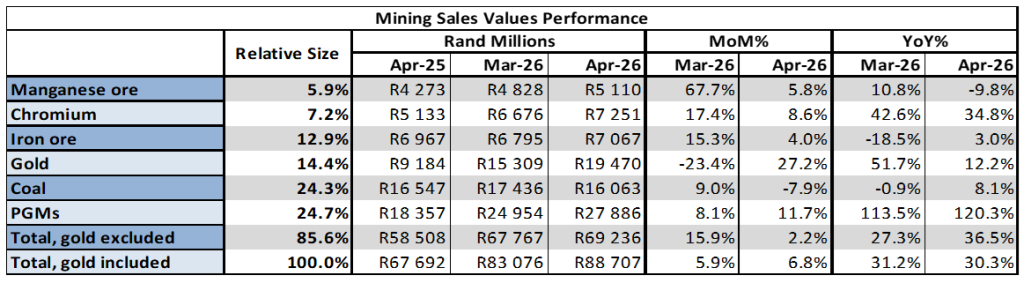

In April 2026, South Africa’s mining activity rose 8.2% following the revised 2.5% increase recorded in March 2026. This growth was predominantly driven by:

- A 36.5% increase in PGM mining production, which contributed 8.8 percentage points to the overall mining output for the month.

- Manganese production rose by 19.0% during April, while adding 1.3 percentage points towards mining production growth and

- A 17.5% increase in Chromium production, which added an additional 1.1 percentage points to total mining output growth for the month.

For the rolling quarter ending April 2026, compared with the previous rolling quarter, seasonally adjusted mining output increased by 2.4%. This increase was primarily due to:

- A 10.5% increase in platinum mining, which increased total mining production by 2.8 percentage points and

- An increase in Gold production, which rose by 8.6% and added 0.8 percentage points for the quarter under review.

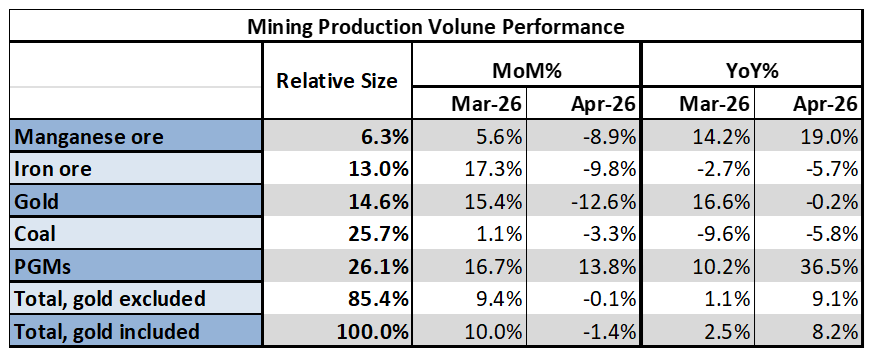

In April, nominal mining sales rose 30.3%. This positive trend was notably supported by:

- A 120.3% surge in platinum sales, which added 22.4 percentage points to overall mining sales growth.

- Another solid 12.2% rise in gold sales, contributing 3.1 percentage points.

- Chromium ore sales, which grew by 34.8%, added another 2.7 percentage points and

- Coal sales, which grew by 8.1% and added another 1.8 percentage points towards overall mining sales growth for April 2026.

The mining sector remains vital to South Africa’s economy, generating foreign exchange and employing approximately 476,000 people, an increase of around 32,000 from the previous quarter, according to StatsSA labour statistics for the first quarter of 2026. According to the latest GDP data, the mining sector grew by 5.7% during the first quarter of 2026, driven by a notable increase in global gold and platinum prices due to the ongoing conflict in the Middle East and the subsequent flight to safe-haven assets such as gold. This sector remains crucial for the South African economy due to the number of people employed within it and in associated auxiliary businesses, and its importance in earning foreign reserves.

However, challenges persist, including concerns over exports to the US following new tariff measures introduced on 7 August, proposed export tariffs on manganese, and import tariffs on steel exports to the Eurozone. The sector also faces challenges related to the loss of AGOA benefits in September and ongoing issues with the new Mining Charter.

Internationally, tensions between the US and China are rising, primarily due to trade disputes and tariff wars. These issues are further complicated by the ongoing conflict in the Middle East, particularly between the US, Israel, and Iran, as well as the closure of the Strait of Hormuz. This situation continues to drive up fuel and production costs for South Africa’s manufacturing and mining sectors in the short- to medium-term, at least.

These geopolitical challenges and the conflict in the Middle East are disrupting global markets and limiting trade, as seen in the data released since the conflict began. However, there is some good news: certain mining materials essential to steelmaking remain temporarily exempt from high US tariffs. This exemption offers some relief to the mining sector, which is vital to South Africa’s economy, providing jobs and foreign exchange and supporting overall growth.