Consumer Inflation – April 2026

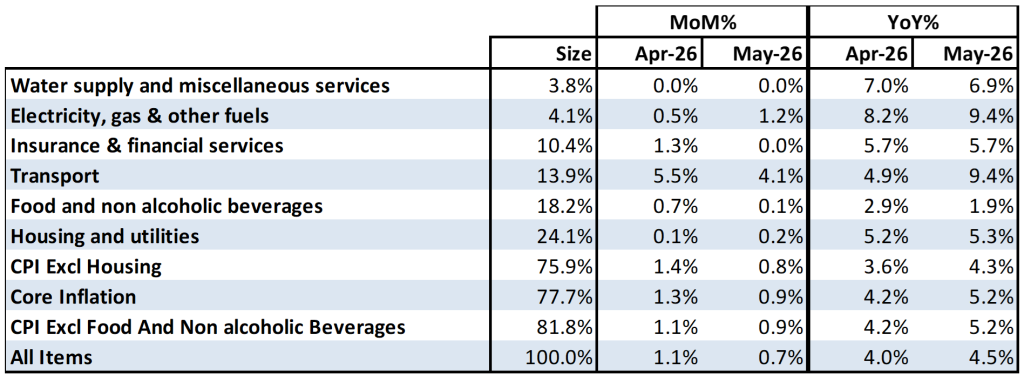

In May 2026, the Consumer Price Index (CPI) rose by 4.5% year-on-year, which is slightly higher than the 4.0% increase recorded in April, yet just below the market’s forecast of 4.7%. This uptick in consumer prices was mainly due to:

- Housing and Utilities: Increased by 5.3%, contributing 1.3 percentage points.

- Transport: Jumped by 9.4%, also contributing 1.3 percentage points.

- Insurance and Financial Services: Went up by 5.7%, adding 0.6 percentage points.

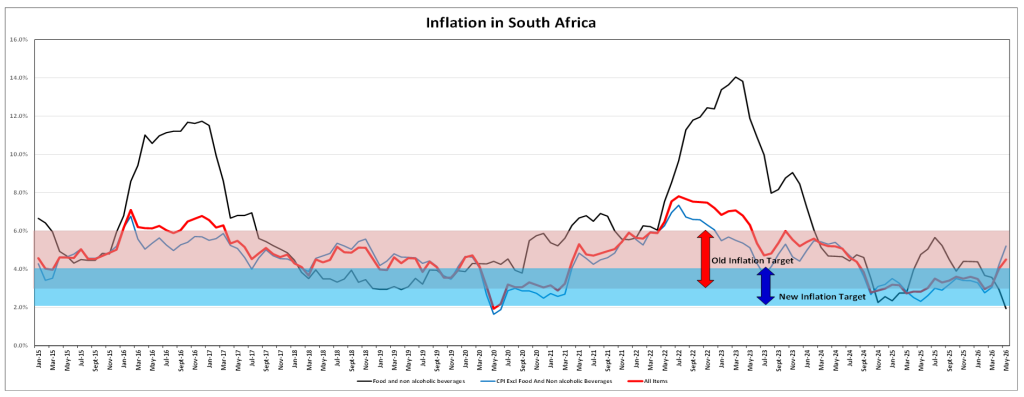

Compared to April, the year-on-year inflation rate for goods climbed from 3.4% to 4.4%. Meanwhile, services inflation rose slightly from 4.6% to 4.7%. Notably, inflation for both goods and services has again surpassed the Reserve Bank’s upper limit of 4.0% within the new target range. This inflationary rise continues to erode household purchasing power in South Africa. Consequently, many consumers and businesses rely more on short-term credit, making them vulnerable to changes in interest rates, exchange rates, global oil prices, and import costs, which in turn affect domestic prices. These vulnerabilities have been exacerbated by the ongoing conflict in the Middle East and the significant increase in fuel prices from April to May, although some relief is expected in June. This scenario is likely to add inflationary pressures in the coming months.

Following the Monetary Policy Committee (MPC) meeting in January 2026, the Reserve Bank chose to keep interest rates unchanged after reviewing January inflation figures and forecasts. However, there was a 25 basis-point increase at the end-of-May meeting due to the recent inflation spike, which stems from the Middle East conflict and rising international oil prices observed in April and May. The elevated fuel and transport costs are anticipated to influence current inflation expectations. The Bank’s cautious stance aims to maintain price stability amid ongoing economic and international uncertainties, including the 30% tariffs imposed by the US on South African exports, which have negatively impacted the manufacturing sector as reflected in the Q4 GDP data. Such uncertainties could also affect the Rand’s value against the US dollar, with expected volatility, particularly with the potential peace deal between the US and Iran and the reopening of the Strait of Hormuz on the horizon.

Due to the consistently high international fuel prices, the South African Reserve Bank (SARB) has temporarily paused the rate-cutting cycle to ensure price stability and anchor inflation expectations. Prior interest rate cuts in late 2024, throughout 2025, and another in November 2025 were aimed at stimulating demand by increasing disposable income for households beyond interest payments, fostering economic growth. However, rising fuel prices may somewhat limit this growth potential.

Despite sustained economic growth of 0.5% in the first quarter of 2026, the Bank remains wary due to persistent global uncertainties. Factors such as inflation, the US-China tariff dispute, and the possibility of future tariffs on BRICS nations could affect price stability. Furthermore, the Middle East conflict may continue to keep international oil prices high if shipping safety cannot be assured through the Strait of Hormuz or if the proposed peace deal collapses and the strait is closed off again. Future interest rate decisions will likely consider moderate inflation within the new target band, slow economic growth, improvements in electricity supply, positive market sentiment, and international tensions impacting oil prices.

In conclusion, maintaining price stability and protecting the Rand’s value are top priorities for South Africa as it navigates the initial months of 2026, amid current international developments and associated uncertainties.