A view on Demand in the Economy: Retail Sales performance – April 2026 Data

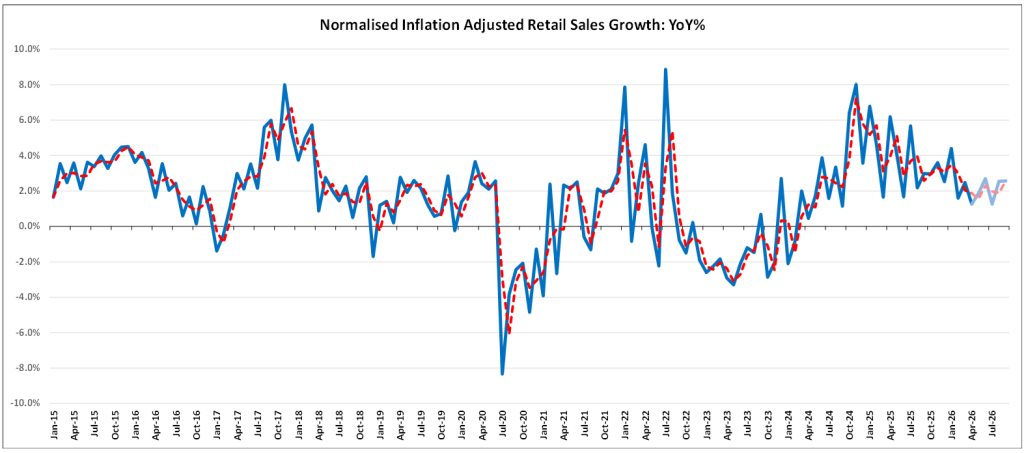

In April 2026, retail sales in South Africa rose by 1.3%, well above the 0.7% analysts had anticipated. This growth underscores a continued but fragile recovery in consumer demand.

Households, however, still face several challenges. The South African Reserve Bank and consumer inflation data point to ongoing increases in administered prices and housing and utility costs, each rising by more than 4.0%, with overall inflation reaching 4.5% in May. Wage growth remains slow amid limited economic expansion, which remains a concern, while uncertainties in international trade, including diplomatic tensions between Washington and Pretoria and the lapse of the African Growth and Opportunity Act (AGOA) in September 2025, have weighed on domestic demand and encouraged cautious spending through late 2025.

April’s 1.3% gain continues the recovery trend from April 2025 to April 2026, even though consumer demand remains fragile but stable at this stage. The April expansion in retail sales is likely still supported by interest-rate cuts and monetary easing implemented between September 2024 and November 2025, but higher fuel costs in recent weeks will weigh heavily on consumer spending in the months to follow, not to mention the increase in interest rates at the SARB’s May meeting. The interest rate increase by the SARB was intended to “combat rising inflation and inflation expectations”, even though these inflationary pressures emanated from outside South Africa and were completely beyond the control of the SARB in Pretoria. The South African Chamber of Commerce and Industry (SACCI) recorded a decrease in business confidence (the index falling from 131.1 in March to 123.6 in April 2026). The FNB/BER consumer confidence index also improved slightly, from -9 in 2025Q4 to -7 in 2026Q1. Even with an improvement in consumer confidence during the first quarter, consumer caution remains persistent. Although inflation is still relatively low and the Reserve Bank reduced rates in January, July and November 2025, the full effects on consumer behaviour will take time to materialise as interest rate changes can take up to 18 months to filter through the economy, given stable fuel prices, but rising fuel prices are going to affect retail sales adversely going forward.

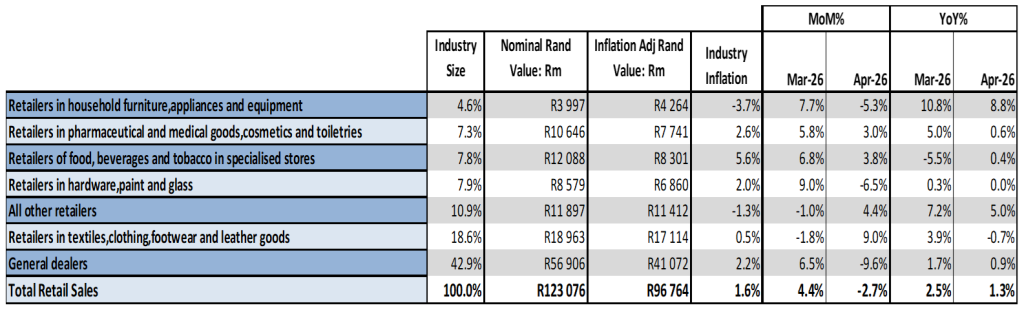

April’s retail growth was driven by:

- Other retailers: up 5.0%, contributing 0.6 percentage points

- General dealers up 0.9%, contributing 0.4 percentage points and

- Retailers in household furniture, appliances and equipment rising by 8,8% and contributing 0.4 percentage points.

The sustained momentum since July suggests a steady, if cautious, recovery. Interest-rate cuts from September 2024 to November 2025 have eased some household financial pressure and still support demand recovery at this stage, but the 25-basis-point interest-rate increase in May, international developments, higher fuel prices, and a possible further increase in interest rates may weigh on consumer demand going forward.