Manufacturing Production – April 2026

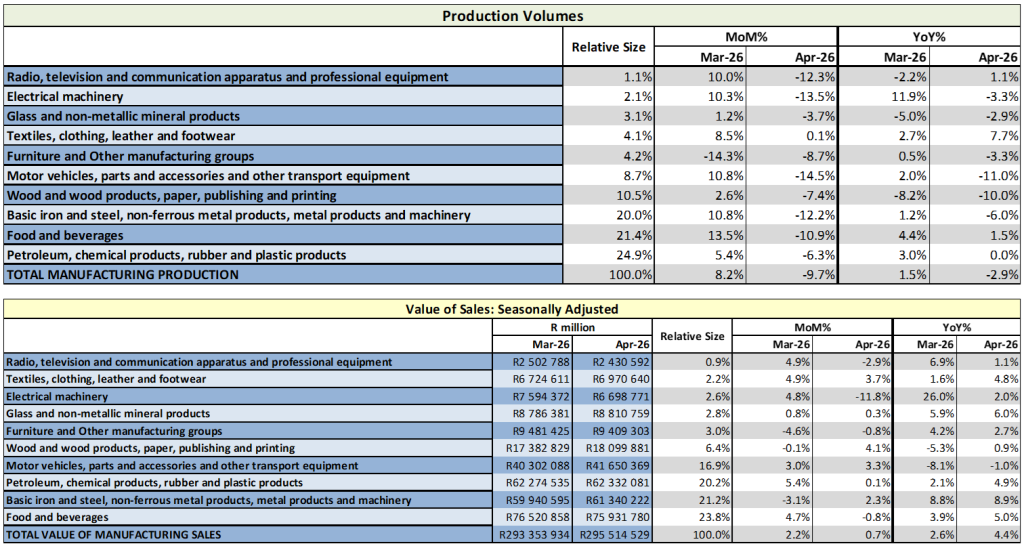

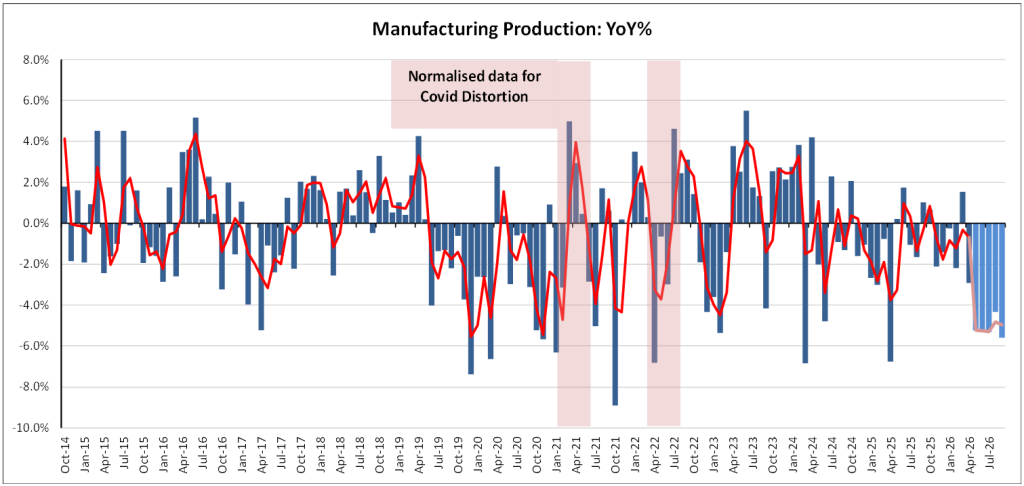

In April 2026, South Africa’s manufacturing output contracted by 2.9%, following the 1.5% increase in March 2026. This decrease is far worse than the 1.2% increase analysts forecast for April 2026. During the same period, the Purchasing Managers’ Index (PMI) increased 3.6 points, from 49.0 in March 2026 to 52.6 in April 2026. This indicates a positive view of the business environment as output expanded within the sector.

The contraction in manufacturing production during April was largely attributed to basic iron and steel, non-ferrous metal products, metal products, and machinery, which decreased by 6.0%, contributing -1.4 percentage points to the overall manufacturing decline. Similarly, the wood and wood products, paper, publishing and printing industry saw a growth decline of 10.0%, subtracting an additional 1.0 percentage points, while the motor vehicles, parts and accessories and other transport equipment industry contracted by 11.0%, subtracting an additional 0.9 percentage points towards manufacturing output during this period. These sectors were significant contributors to the industry’s underperformance in April.

Seasonally adjusted manufacturing production decreased by 1.3% for the rolling quarter ending April 2026 compared to the previous rolling quarter. Out of ten sectors, six reported contractions during this period. Significant contractions included:

- Petroleum, chemical products, rubber and plastic products, declined by 3.5%, subtracting 0.8 percentage points from growth.

- Wood and wood products, paper, publishing and printing, which decreased by 3.4%, also contributed a 0.3 percentage point reduction.

Seasonally adjusted manufacturing sales increased by 2.3% during the rolling quarter ending April 2026 compared to the previous rolling quarter. Significant increases occurred in:

- Basic iron and steel, non-ferrous metal products, metal products and machinery, which increased by 5.7%, adding 1.2 percentage points towards sales growth for the quarter.

- The motor vehicles, parts and accessories and other transport equipment division, which rose by 7.1%, added another 0.9 percentage points towards sales growth for the quarter under review.

Manufacturing is a critical component of South Africa’s economy, employing approximately 1.58 million people and accounting for 12.5% of the GDP in 2025. Employment slightly increased from 1.548 million in Q4 2025 to 1.587 million in Q1 2026. GDP figures for the fourth quarter indicate a 0.6% quarterly decrease in manufacturing output, suggesting that US trade tariffs since August 2025 have caused some distress in the manufacturing sector by eroding price competitiveness in the US market, driven by higher import prices due to tariffs on South African-produced export goods. It should, however, be noted that exports to the US market have declined by 56% since 2025 due to tariffs, trade tensions and diplomatic “disputes” between Pretoria and Washington.

As a result of trade tariffs with the US and ongoing diplomatic tensions between Pretoria and Washington, business owners remain cautious, as evidenced by the April 2026 PMI data, which is just above the positive 50-point threshold. However, companies are still maintaining substantial cash reserves of approximately R1.8 trillion, up from R1.1 trillion in the first quarter of 2025, according to the Reserve Bank. This reflects a prudent approach amid current domestic and global economic uncertainties in the short- to medium-term.